Why do domestic fuel prices fluctuate even when global crude markets seem stable? Moving beyond politics and basic inflation, this article provides students with a technical deep-dive into the complex algorithms, currency hedging strategies, and fiscal structures that determine retail fuel pricing in India.

In India, petrol and diesel are deregulated commodities (since 2010 and 2014 respectively), meaning the government does not directly set retail prices. Instead, Oil Marketing Companies (OMCs) like IOCL, BPCL, and HPCL determine prices based on specific technical parameters.

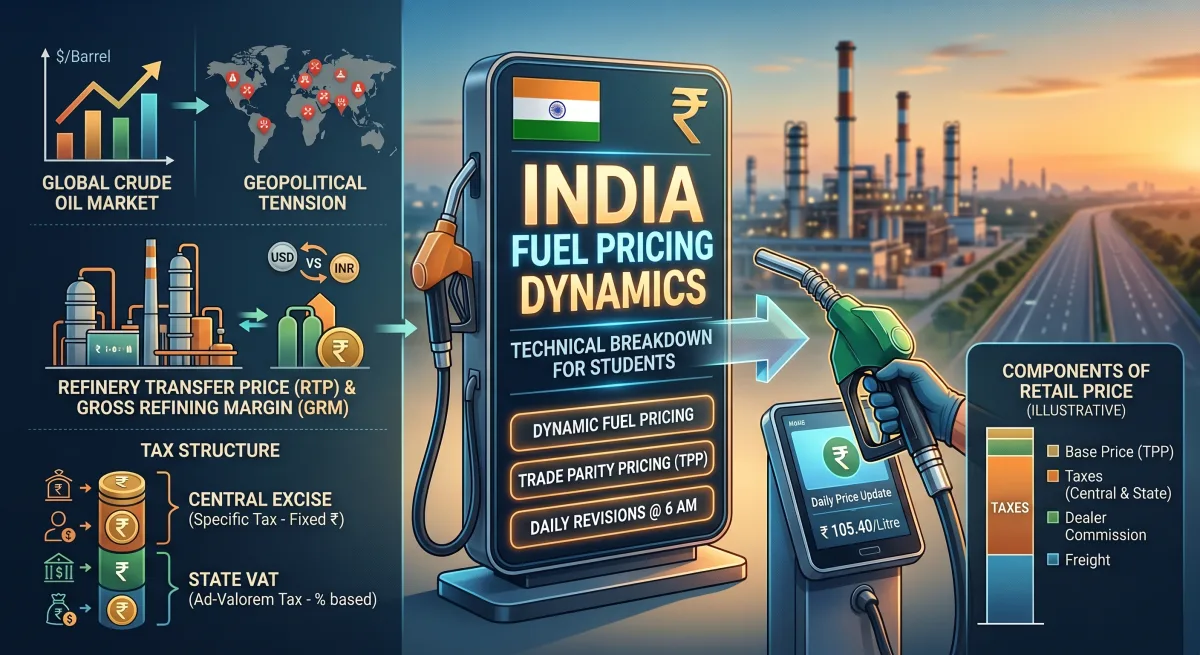

Here is the comprehensive technical breakdown of how fuel pricing works:

1. Dynamic Fuel Pricing (Daily Pricing Mechanism)

India uses a system called Dynamic Fuel Pricing, introduced to move away from fortnightly (15-day) price revisions.

- The Mechanism: OMCs recalculate the retail price of fuel every single day at 6:00 AM.

- The Parameter: This price is based on a rolling average of the international benchmark prices of petrol and diesel over the preceding 15 days, combined with the daily fluctuations of the foreign exchange rate.

- Academic Significance: This mechanism ensures that micro-movements in the global energy markets are immediately absorbed by the domestic market, preventing a sudden shock or lag in the fiscal ecosystem.

2. Trade Parity Pricing (TPP)

This is the foundational pricing model used in India. The base price of fuel is not calculated purely based on raw crude oil prices; rather, it is derived using the Trade Parity Pricing (TPP) formula.

The TPP is a weighted average formulated as:

TTP = (80% * Import Parity Price) + (20% * Export Parity Price)

- Import Parity Price (IPP): The theoretical cost that would be incurred if India were to import refined petrol or diesel directly from international refineries. It includes the Free on Board (FOB) price of the refined product, ocean freight charges, insurance, port dues, and custom duties.

- Export Parity Price (EPP): The benchmark price Indian refineries would receive if they exported their refined petroleum products to the international market.

Student Note: Even though India imports raw crude oil, it possesses a massive domestic refining capacity. Therefore, the 80:20 ratio acts as an economic balance between what it costs to buy from abroad versus what domestic refiners can earn by exporting.

3. Refinery Transfer Price (RTP) & Gross Refining Margin (GRM)

Before fuel reaches the distribution network, it undergoes processing at domestic refineries (e.g., Jamnagar, Digboi, or Mumbai).

- Refinery Transfer Price (RTP): This is the price charged by refineries to the OMCs to transfer the processed fuel. RTP is determined based on the TPP framework mentioned above.

- Gross Refining Margin (GRM): For students tracking energy economics, GRM is a critical KPI (Key Performance Indicator). It represents the difference between the total value of petroleum products produced by a refinery and the price of the raw crude oil used to produce them:

GRM = Value of Refined Products per barrel - Cost of Crude Oil per barrel

High global demand for refined products inflates the GRM, which can push domestic base prices upward even if raw crude prices remain relatively stable.

4. Specific vs. Ad-Valorem Taxation

The retail price of fuel is heavily driven by its tax structure. Since petroleum products are currently kept outside the purview of the Goods and Services Tax (GST), they face a dual-taxation layer that operates under two distinct economic concepts:

- Specific Tax (Central Excise Duty): Administered by the Central Government, this is a fixed monetary levy per litre of fuel (e.g., a fixed ₹20 or ₹25 per litre). It does not fluctuate regardless of whether global oil prices rise or fall.

- Ad-Valorem Tax (State VAT/Sales Tax): Administered by individual State Governments, this tax is levied as a percentage of the base value (e.g., 20% or 30% of the price charged to the dealer).

- The Cascading Effect: Because State VAT is ad-valorem, any increase in global crude oil prices automatically expands the absolute tax amount collected by the states, creating a compounding effect on inflation at the pump.

[Base Price + Freight] ──> + Central Excise (Specific/Fixed) ──> + State VAT (Ad-Valorem/Percentage) ──> Final Retail Price

5. Under-Recoveries vs. Fiscal Subsidies

In times of extreme geopolitical stress (like the current Middle East/Iran supply-side bottleneck), global oil prices skyrocket. If OMCs are discouraged or restricted from raising retail prices to protect consumers from inflation, a fiscal gap emerges.

- Under-Recoveries: This is the technical term for the revenue loss incurred by OMCs when the domestic retail selling price falls short of the imported cost (the break-even parity price).

- Fiscal Subsidies / Oil Bonds: If the government chooses to compensate OMCs for these under-recoveries using budgetary allocations or issuing long-term sovereign securities (Oil Bonds), it becomes a fiscal subsidy liability.

6. Currency Volatility and Forex Hedging

Because international oil trade is denominated in Petrodollars (USD), India’s Current Account Deficit (CAD) is highly sensitive to fuel pricing.

- The Exchange Rate Vector: If the Indian Rupee (INR) depreciates against the USD, importing oil becomes more expensive in domestic currency terms, even if the price of a global barrel of crude oil remains unchanged.

- Hedging: To mitigate the financial risk of currency volatility, OMCs frequently employ forex hedging strategies. They use derivative instruments (like futures and options contract markets) to lock in currency exchange rates in advance, stabilizing their financial exposure against unpredictable global market swings.